Introduction

The rise of social media has created a new class of financial content creator - the 'finfluencer' - who shares investment opinions, stock tips, and portfolio strategies to audiences that sometimes number in the millions.

While financial education and market awareness serve a valuable public purpose, SEBI has become increasingly concerned about the point at which content creation crosses into unregistered investment advisory activity.

Since August 2023, SEBI has progressively tightened its regulatory framework for finfluencers through a series of circulars. The August 2023 circular restricted registered intermediaries (including brokers, AMCs, investment advisers, and research analysts) from associating with unregistered persons who provide advice or recommendations about securities. An October 2024 circular extended these restrictions further. Most significantly, a January 29, 2025 circular introduced an additional restriction: finfluencers engaged in education may only use stock price data with a three-month lag, effectively barring real-time trading tips disguised as education. The January 2025 circular also expanded the association restrictions to cover mutual fund distributors, PMS distributors, and AIF distributors. SEBI has also demonstrated willingness to take strong enforcement action: in December 2025, SEBI issued an interim order against a prominent trading academy, directing disgorgement of approximately Rs 546 crore in what was characterised as an unregistered investment advisory operation masked as education. These developments represent a clear regulatory direction for both finfluencers and the fintech platforms that work with them.

Who Is a Registered Investment Adviser (RIA)?

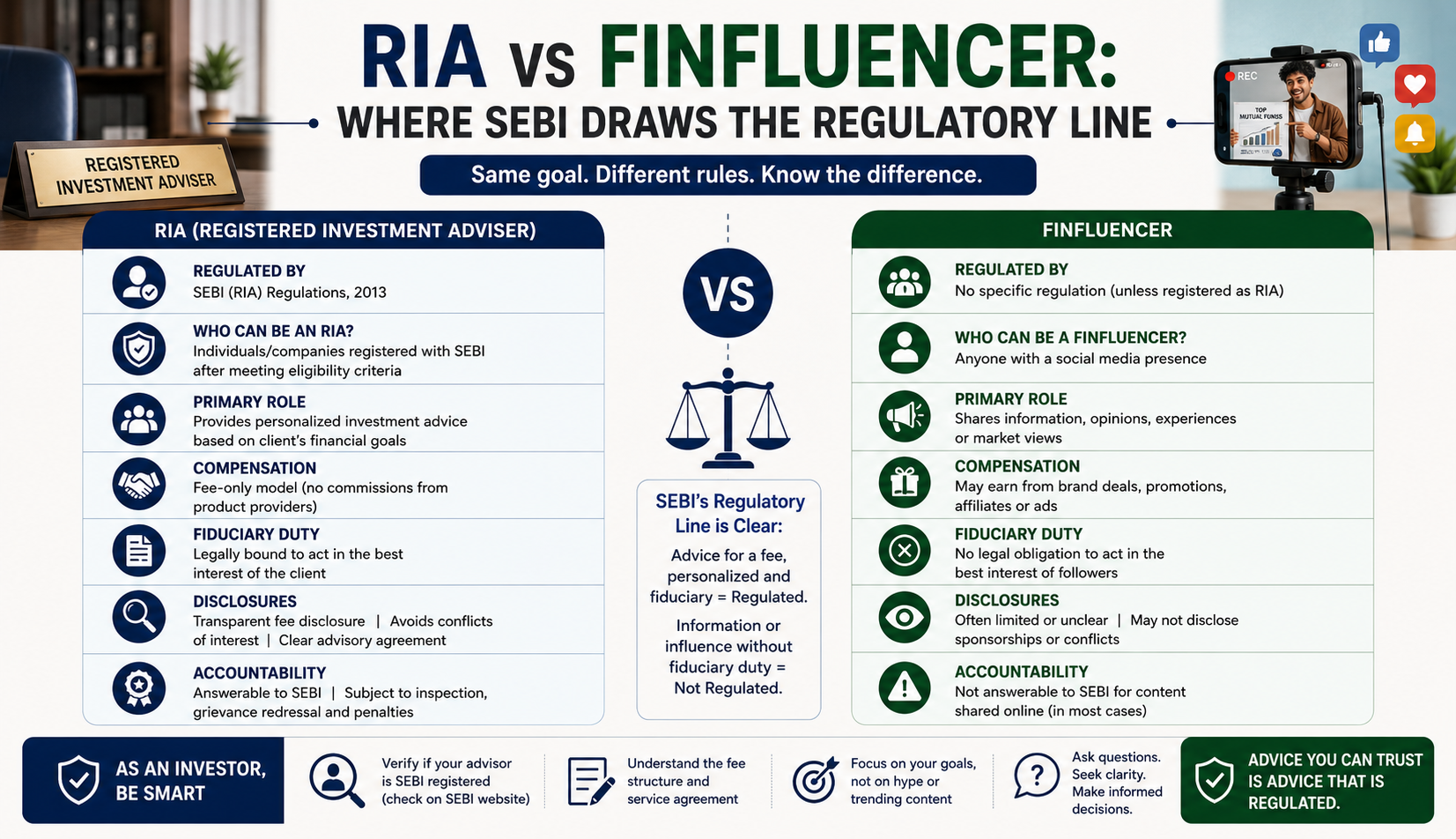

A Registered Investment Adviser is registered with SEBI under the SEBI (Investment Advisers) Regulations, 2013. RIAs are required to act in a fiduciary capacity and are subject to ongoing compliance obligations including:

• Formal client risk profiling and documented suitability assessments

• Written advisory agreements and fee disclosures

• Prohibition on earning commissions from product manufacturers

• Segregation of advisory and distribution activities

• Audit and SEBI compliance reporting

RIAs provide personalised investment advice based on individual client circumstances and are accountable for the suitability of their recommendations. Their regulated status is verifiable on SEBI's public registration database.

Who Is a Finfluencer?

A finfluencer is a social media creator who produces financial content - market commentary, investment opinions, personal finance education, trading strategies, or product reviews. Finfluencers are typically not registered with SEBI and operate outside the formal investment advisory regulatory framework.

The finfluencer category spans a wide spectrum - from those providing genuinely educational content with appropriate disclaimers to those effectively issuing buy/sell calls to large follower bases, sometimes in exchange for undisclosed payments from brokers, AMCs, or listed companies.

Where SEBI Draws the Line

SEBI's regulatory concern is not about financial education per se. The regulatory line is crossed when:

• Content constitutes personalised investment advice - recommendations tailored to individual financial circumstances rather than general market commentary

• Specific buy/sell/hold calls are made regarding particular securities or funds without SEBI registration

• The finfluencer receives consideration (money, gifts, commissions, or equity) from entities whose securities or products they recommend, without disclosure

• Subscription-based groups or communities are operated where trading calls, portfolio recommendations, or investment strategies are sold - this constitutes investment advisory activity and requires RIA registration

• Claims of guaranteed returns, assured profits, or risk-free investment are made

The pump-and-dump scheme - where a finfluencer accumulates a position in a security, promotes it to their audience to drive up the price, then sells - is a criminal offence under Section 12A of the SEBI Act, 1992 and Regulation 4 of the SEBI (Prohibition of Fraudulent and Unfair Trade Practices) Regulations, 2003.

SEBI’s Evolving Finfluencer Framework (2023–2026) - Impact on Regulated Intermediaries

SEBI's August 2023 circular on association with unregistered entities has important compliance implications for regulated intermediaries (brokers, AMCs, RIAs, research analysts). These entities:

• Cannot use finfluencers who provide securities advice or recommendations for marketing, referrals, or endorsements

• Cannot share revenue with or pay commissions to unregistered persons in connection with investment advisory or research activities

• Must ensure all influencer marketing relationships are with persons who are either not providing securities advice, or who are properly registered with SEBI

Non-compliance exposes the regulated intermediary to SEBI enforcement action including suspension of registration, financial penalties, and public censure.

Compliance Risks for Fintech and Wealth-Tech Platforms

Influencer marketing due diligence

Fintech platforms that use influencers to promote investment products, trading platforms, or advisory services must conduct due diligence to ensure the influencer is not providing unregistered investment advice in connection with the engagement. Marketing campaigns should be reviewed by compliance teams before

launch.

Affiliate programme design

Performance-based affiliate programmes that reward influencers per account opened or investment made can blur the line between referral marketing and distribution/advisory activity. Programme design should be reviewed against applicable SEBI and RBI requirements.

Platform liability

Digital platforms that host or amplify investment-related content - even without direct involvement in its creation - may face scrutiny if the content constitutes unregistered advice and the platform benefits financially from it.

AI-generated recommendations

Algorithmic nudges, robo-advisory features, and AI-generated investment suggestions raise similar classification questions. If the algorithm provides personalised recommendations about specific securities or funds, SEBI may take the view that the platform is providing investment advisory services requiring registration.

Practical Guidance for Finfluencers

• Ensure all content that could constitute investment advice is disclaimed as general educational content

• Disclose all commercial relationships with financial product manufacturers, brokers, or platforms in every post or video

• Do not operate subscription services offering trading calls or portfolio recommendations without SEBI RIA registration

• Do not make claims of guaranteed returns, assured profits, or consistently beating the market

• Register with SEBI as an RIA or Research Analyst if providing personalised investment advice or research recommendations

Practical Guidance for Fintech Platforms

• Review all influencer contracts for compliance with the SEBI August 2023 circular before engagement

• Build a marketing review process that includes compliance sign-off for all financial promotions

• Maintain documentation of influencer due diligence and content approvals

• Assess whether any algorithmic or AI features on the platform constitute investment advisory services under the IA Regulations

• Train marketing teams on the distinction between brand promotion and regulated financial communication

Conclusion

The RIA vs finfluencer debate reflects a broader regulatory challenge: how to protect retail investors in a world where financial information reaches millions through social media without the safeguards built into traditional regulated advisory frameworks. SEBI's August 2023 circular signals clearly that the regulator is drawing stricter boundaries. For finfluencers, registered intermediaries, and fintech platforms, understanding and respecting those boundaries is both a legal obligation and a prerequisite for sustainable business operations.

At KP Regtech, we help fintech businesses, RIAs, startups, and regulated entities build practical compliance frameworks, digital governance systems, and regulatory documentation aligned with evolving SEBI and financial sector expectations.